5 Things We Learned This Week - 3/23/2025

March 22, 2025

The S&P 500 rose 0.4% this week, snapping a four-week losing streak. The Bloomberg Aggregate Bond Index rose 0.5%, Gold rallied 1.2% and Bitcoin fell 0.9%.

The Leading Economic Index declined -0.3% in February, weighed down by falling expectations for future business conditions and a decline in manufacturing new orders. The Existing Home Sales report jumped 4.2% versus the prior month, but sales activity is still down year-over-year. Unsold inventory is up 17% compared to this time last year. The Fed left interest rates unchanged on Wednesday for a second straight meeting. Officials stuck to their previous forecast for two more rate cuts this year despite bracing for higher inflation and slower growth. Fed chair Jerome Powell said that further progress on inflation may be delayed because of tariffs.

Market Technical Update

US equities have stumbled in Q1, but evidence continues to point to a likely short-term respite. After this week's modest gain in the S&P 500, investor sentiment still resides in deeply oversold territory. The AAII Bull-Bear Survey is showing a net bullish reading of just 21%—well below its historical average of 38%. As Warren Buffett says, "Buy when others are fearful." Meanwhile, insider buying has improved. The insider sentiment index shows the buyer-to-seller ratio has risen to 0.46, the highest since June and near historical averages. Insider buying is powerful because executives know the present state of their firms best, and high insider activity has preceded rebounds.

As we wrote about last week, quarter-end rebalancing by target-date funds could further bolster markets as these funds shift allocations—potentially buying equities after recent declines. The magnitude of rebalancing won't be as large as some recent episodes that marked key market bottoms (i.e. March of 2020), because equities aren't down as much this quarter. But passive investors are easy to telegraph, and we know they'll be scooping up shares this week. Since the stars appear aligned for a tactical rally, Silverlight managed accounts are no longer positioned maximally defensive. The next hurdle for stocks will be Q2 earnings season, starting unofficially with JPMorgan’s report on April 11.

Liquidity Risk Looms

Debt isn’t inherently evil, but too much debt with too little liquidity is a recipe for chaos in today’s refinancing-driven markets. Michael Howell’s latest piece flags a looming threat: a debt maturity wall from the COVID-era zero-rate days. The peak for maturities will be in 2027, but refinancing pressure will start to accelerate by mid-2025. The Fed didn't do much to alleviate concerns about this issue at the March FOMC meeting. The committee held rates steady, hinted at 50 basis point cuts, and trimmed QT from $25 billion to $5 billion—largely overlooking money market tensions.

Howell’s Fed Liquidity metric projects a peak in August 2025, then a drop below a $3.25 trillion “minimum reserve” threshold by September. That’s a red flag for regional banks and repo spreads. Despite a $612 billion liquidity boost since late-2024, the Fed’s reluctance to expand its balance sheet—or restart QE—risks a crunch. Investment takeaway? Silverlight will remain strategically underweight risk assets until the liquidity outlook improves. We can tactically trade oversold conditions, but the market needs another liquidity surge to generate a sustainable rally.

When the Market Falls, the Magnificent 7 Stocks Lag

The mega cap stocks that dominate the S&P 500 are often lauded as low-risk investments due to their monopoly like features. However, this label isn't supported by the data. Low-risk investments are supposed to outperform on the downside, but Mag 7 stocks do the opposite.

The market darlings known as the Magnificent 7 have recently lost their luster, with Goldman Sachs' David Kostin dubbing them the "Maleficent Seven." These high-beta stocks, which have driven much of the S&P 500's gains, are now proving to be a double-edged sword for investors. While the Magnificent 7 outperform during bull markets, they tend to underperform significantly in corrections. This high-beta characteristic makes them a poor fit for risk-averse investors.

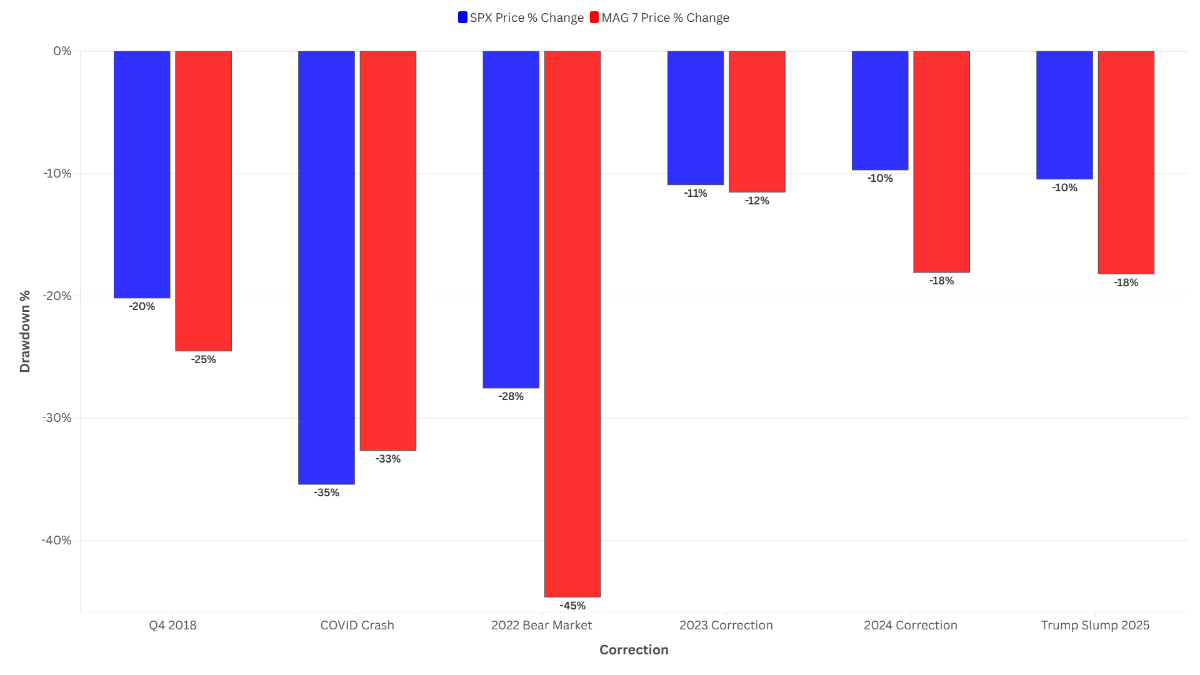

Here’s a snapshot of how the Magnificent 7 (equal-weighted) stacked up against the S&P 500 (SPX) during recent corrections. Mag 7 has lagged in every correction other than the Covid Crash, which uniquely benefitted mega cap tech firms:

Q4 2018 (Oct 3 - Dec 26): Mag 7: -24.5%, SPX: -20.2%

Covid Crash (Feb 19 - Mar 23): Mag 7: -32.7%, SPX: -35.4%

2022 Bear Market (Jan 4 - Oct 13): Mag 7: -44.6%, SPX: -27.5%

2023 Correction (Jul 27 - Oct 27): Mag 7: -11.5%, SPX: -10.9%.

2024 Correction (Jul 16 - Aug 5): Mag 7: -18.1%, SPX: -9.7%.

Trump Slump 2025 (Feb 19 - Mar 13): Mag 7: -18.2%, SPX: -10.5%.

The S&P 500's increasing concentration in these stocks—recently comprising over 35% of the index—poses a significant risk. Their elevated valuations make them vulnerable in corrections. The other key thing to understand with these stocks is they are disproportionately owned by nearly everyone. That means when the broad stock market goes up, these stocks will probably go up more, and when the broad stock market goes down, these stocks will probably go down more.

Formula 1’s Netflix Win Fuels Silverlight’s Investment

The 2024 Formula 1 season roared to a close as a blockbuster for Netflix, with Drive to Survive Season 6 amplifying the sport’s drama and drawing record U.S. viewership. ESPN reports average race audiences hit 1.2 million, up from 1.1 million in 2023, cementing F1’s stateside surge. Netflix’s behind-the-scenes magic turned drivers into stars, supercharging fan engagement and Liberty Media’s Formula One Group (FWONK) revenue, which climbed 13% to $3.65 billion in 2024.

This week, Silverlight managed accounts invested in FWONK shares. F1’s strategic edge lies in its global expansion—think Miami, Vegas—and media-savvy storytelling. Another catalyst involves a likely corporate restructuring that should allow FWONK to enter the major indices and benefit more from passive flows. Its economic moat? A unique blend of scarcity (one league, not a team) and sticky sponsorships from Heineken to Rolex. The outlook shines bright: new races, rising broadcast deals (Netflix may bid $2 billion for US rights), and a fanbase hooked on high-octane narratives. Silverlight believes operating margins can rise due to inflation in sports media rights, a longer race schedule, and better monetization of sponsorship and merchandising opportunities. We see Formula 1 as a sturdy investment likely to compound in value over the coming years.

World Happiness Report Highlights

The 2025 World Happiness Report is out, and it's packed with fascinating insights. Here are three standouts that caught our attention:

The power of kindness: People consistently underestimate the benevolence of others. Lost wallet return rates are nearly double what most expect, highlighting our overly pessimistic view of humanity.

Meal sharing matters: Dining with others is strongly linked to wellbeing across all regions. However, the US has seen a 53% increase in solo diners over the past two decades. This trend could be impacting our collective happiness.

US happiness is in a bear market: America has fallen to its lowest-ever ranking (24th) in global happiness. This decline coincides with decreasing social trust, potentially fueling political polarization.

Finland ranks as the happiest country due to its strong social support, high trust in institutions, and robust welfare system providing free healthcare and education. Low income inequality, economic stability, and excellent work-life balance boost wellbeing. Access to nature, a sense of community, and low corruption further enhance contentment.

These findings underscore a crucial lesson: our perceptions and social connections profoundly impact our happiness.

This material is not intended to be relied upon as a forecast, research or investment advice. The opinions expressed are as of the date indicated and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and non-proprietary sources deemed by Silverlight Asset Management LLC to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Silverlight Asset Management LLC, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any of these views will come to pass. Reliance upon information in this post is at the sole discretion of the reader.