When Cash Is King

Investor cash levels are near an all-time low. Meanwhile, Warren Buffett is sitting on a record amount of cash.

How much cash do you have on the sidelines? How much should you have?

***

Cash competes with other asset classes for investor wallet share. Right now, it’s losing that battle. In the latest weekly survey of Bank of America Merrill Lynch high net worth clients, cash allocation fell to an all-time low of 10.4%. The previous low of 11% was recorded in April 2007.

Cash does not appear to be an attractive asset if you know how to apply The Rule of 72—a math shortcut that allows you to figure out how long it will take to double your money at a specified level of return.

Once upon a time, cash paid 5%. Really, it did. Back then, you could park in cash and double your money in 14.4 years (72/5 = 14.4).

Presently, cash yields very little. You can get 1% or so.

That's 72 years to double your money!

If you haven’t figured out yet why people have rushed out of bonds and cash toward stocks, now you know.

Cash at 1% appears to most investors to be a liability. That is, if you consider opportunity cost or inflation, cash isn’t king—it’s more of a court jester.

And yet the all-time ‘King of Investing,’ Warren Buffett, is compiling the biggest cash war chest in Berkshire Hathaway history.

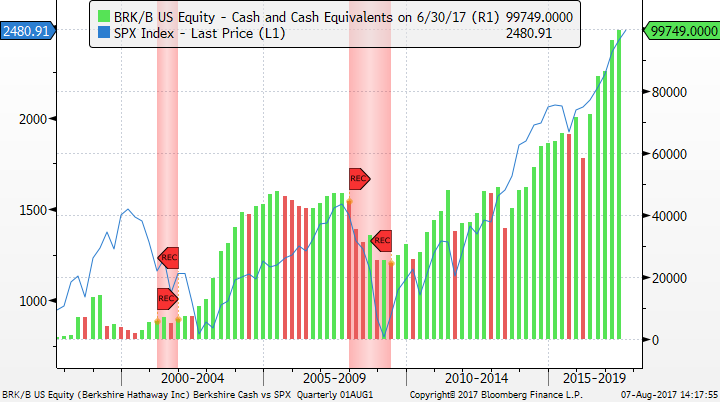

Berkshire’s cash has grown five quarters in a row (see green bars in chart below) and resides near $100 billion, while the S&P 500 (blue line) has steadily advanced over the same period, to an all-time high.

High cash levels are a drag on Berkshire’s earnings. As cash continues to build, some investors and analysts are growing impatient. They want it deployed for a higher return.

He may buy something, but it wouldn’t be Warren Buffett’s normal style to chase the market. If you look closely at the graph, you’ll note he likes to raise cash during bullish climates (i.e. the green bars are more common when the blue line is rising) and spend aggressively in bearish climates (when the blue line is falling). This behavior is totally consistent with his “Be greedy when others are fearful and fearful when they are greedy” mantra.

Buffett practices a form of time arbitrage—meaning that in a world where most people hyper-obsess about short-term returns, he achieves better results with less risk by taking a longer-term view. He’ll endure the short-term pain of low returns if it is the necessary path to achieve higher returns later.

Buffett understands the scarcity value associated with cash. If you are positioned to deploy cash into distressed assets when other investors are scrambling in unison to sell, then you not only limit your downside exposure—which helps compound higher returns in of itself—but you also achieve very attractive entry points on new asset purchases.

However, you can only get to that position if you do what is hard first. That is: raising cash or hedging when market conditions are favorable.

Higher markets and risk levels. While Warren Buffett usually swims countercurrent to the market, most investors do the opposite. As countless Dalbar studies have shown, the average stock or bond investor underperforms by risking up and down at the wrong times.

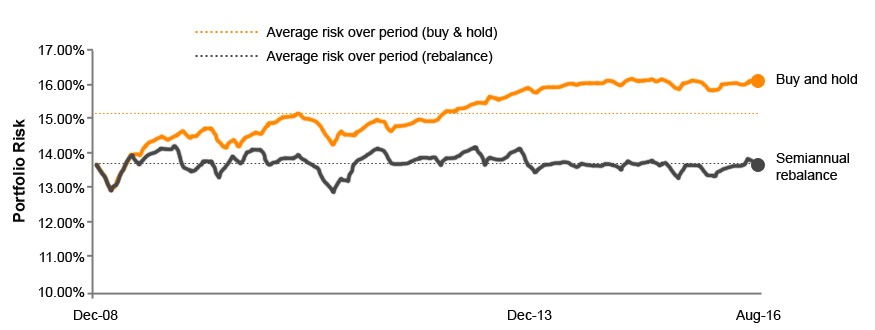

Buy and hold investors don’t necessarily maintain static risk levels, either. If you haven't rebalanced your portfolio over the last few years, you may be surprised at how much additional risk you are now taking on. The illustration below shows how a conventional diversified portfolio can see it’s risk profile drift higher over the course of a bull market (source: Fidelity).

Taking on more risk than your situation warrants becomes especially dangerous in a late-cycle environment.

Rich Dad Poor Dad author, Robert Kiyosaki, defines an asset as something that puts money into your pocket, while a liability is something that takes money out of your pocket. Stocks, bonds, and cash all put money into your pocket over time, but they do so at different times. And any asset can morph into a liability if the allocation is ill-timed.

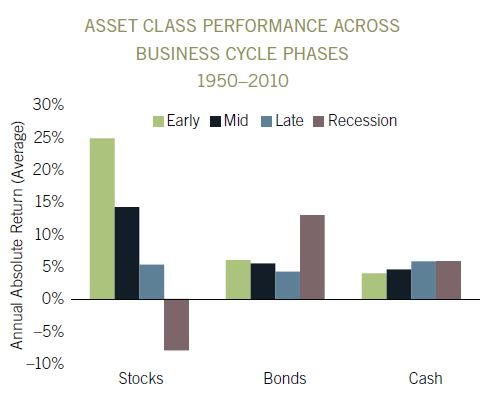

Below is a useful study Fidelity put out a few years ago. It shows the relative appeal of the three major asset classes at different market cycle stages.

Cash becomes a progressively more appealing option as a cycle ages. Stocks, on the other hand, are most appealing at the front-end of a cycle.

It’s been 9 straight years of gains for the S&P 500, so it's hard to fathom we aren’t closer to the end than the beginning.

Hence, now is a valuable time to remember: It’s not how much you make in a bull market that counts, but how much you preserve and roll into the next cycle.

“Every decade or so, dark clouds will fill the economic skies, and they will briefly rain gold. When downpours of that sort occur, it's imperative that we rush outdoors carrying washtubs, not teaspoons.” - Warren Buffett, Letter to Berkshire Hathaway Shareholders, 2017

The best investment opportunities are when others are scrambling to raise cash, when everyone else is selling and you are in the rare position to buy. That’s when cash is at its peak value as an asset—that’s when cash is king.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date indicated and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by Silverlight Asset Management LLC to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Silverlight Asset Management LLC, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any of these views will come to pass. Reliance upon information in this post is at the sole discretion of the reader.