5 Things We Learned This Week - 7/5/2026

July 5th, 2026

The S&P 500 rose 0.6% on a holiday shortened week. The Bloomberg Aggregate Bond Index fell 0.4%, while Gold rallied 2.6% and Bitcoin rose 2.0%.

June nonfarm payrolls rose just 57,000, well short of the 115,000 consensus estimate, and May was revised down to 129,000 from 172,000. The ISM Manufacturing PMI also came in soft, easing below the 54.0 consensus. The labor market printed a soft spot but did not break. Initial jobless claims came in at 215,000, above the 211,000 consensus and the highest reading in more than a month. Continuing claims also came in a touch above the estimate. These are signs of economic deceleration, but are not worth getting too riled up about at this stage.

The market's other job this summer is getting to know Kevin Warsh. Every new Fed chair spends the early months being tested by markets, and this week Warsh held a hawkish line even after the weak jobs print, warning that "prices are too high" and signaling comfort with another rate hike this year. History says this stretch matters. Volcker inherited an inflation problem in 1979 and had to prove he would break it. Greenspan got the '87 crash inside his first ninety days. Bernanke walked into a housing market that was already cracking in 2006. Powell was tested by a fourth-quarter selloff in 2018. The first year of a chairmanship is when the market learns whether the words match the reaction function.

Weak data plus a hawkish chair is the setup. Watch how Warsh responds if the labor cooling continues into July.

SilverSignal's First Quarter On The Field

Silverlight's separately managed account strategies delivered strong performance in the first half of 2026. Core Equity and Dobermans of the Dow both posted double-digit net returns that eclipsed the S&P 500's return of 10.2%. Compounders, which we launched at the start of 2026, was the top performer.

Compounders exists to maximize long-term returns. In Q1 we managed it as a discretionary swing trading strategy. Starting in Q2, SilverSignal became the primary driver of buys and sells. After switching to more of a quantitative trading approach, the portfolio rose 32.9% for the quarter. That is the highest quarterly return in the firm's history, and more than double the S&P 500's gain of 15.2% over the same period. From the day we introduced SilverSignal to you on May 24 through quarter-end, Compounders returned 10.3% against 0.5% for the S&P.

A quarter is only a quarter, and past performance does not guarantee future results. That said, we reiterate what we wrote in that same post: "The backtested forward returns for SilverSignal are the strongest of any model we've built."

We have begun integrating SilverSignal into how we manage Core Equity and Dobermans of the Dow. Using the model more will increase turnover, which for taxable accounts means higher trading costs and more short-term gains. We believe the excess return potential warrants pursuing a higher frequency rebalancing strategy. If more frequent rebalancing does not continue to produce worthwhile results, we will adjust our strategy accordingly. As Story #3 this week explains, net returns are the name of the game.

The other reason we are adapting is that we view the modern stock market as more of a trading market than an investing market. Prices are currently set at the margin by flows and positioning more than by fundamentals, and that rewards active repositioning.

Our outlook for the rest of the year: higher volatility into the midterms, but the overall setup looks constructively bullish. Matt and Michael will host an Investment Outlook webinar covering our macro view and key themes. We will also share a deeper look at how SilverSignal will drive portfolio decisions from here.

Disclosure: Silverlight Asset Management, LLC is an California-registered investment adviser. Composite returns are net of fees, unaudited, and may not reflect individual client experience. SilverSignal backtests are hypothetical. Past performance does not guarantee future results. All investing involves risk of loss.

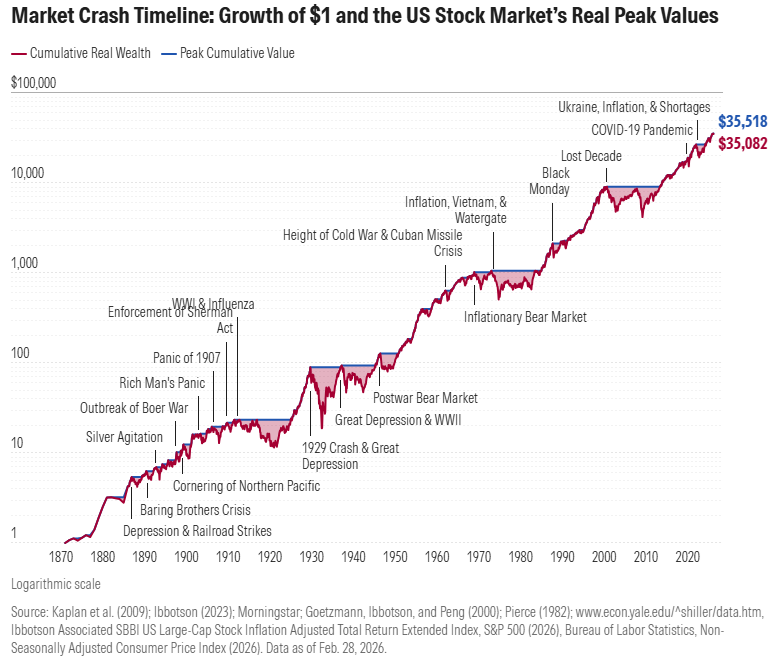

Never Bet Against America

One dollar invested in the U.S. stock market in 1870 would be worth about $35,000 today. That single number is the whole American Exceptionalism thesis in one line.

Warren Buffett has said it plainly: no one has ever built lasting wealth by betting against America. The long-term chart makes the case for him. Stocks have compounded through world wars, the Great Depression, stagflation, 2008, and the pandemic. Over any long horizon you choose, common stocks have out-compounded every other major asset class.

That track record is not luck. It rests on three interlocking pillars.

Rule of law. Stable institutions and enforceable property rights let investors commit capital for decades instead of years.

Market-priced capital. Free-market allocation moves money to the most promising ideas faster than any centralized system on the planet.

A culture of reinvention. Top universities, an entrepreneurial risk appetite, and a steady inflow of global talent produce the breakthroughs that start each new growth cycle.

Every generation gets its crisis, and each crisis is treated as the exception that finally breaks the pattern. It never does. America's system rewards problem-solvers who adapt over incumbents who double down. Short-term pessimism, whether about debt or geopolitics, has repeatedly underestimated the country's capacity for reinvention.

The current worry list is real. Public debt is high. So is political noise. Both are manageable with adult leadership. Meanwhile, U.S. advantages in technology, energy abundance, and talent attraction keep widening.

The lesson for investors is uncomplicated. Stay invested. Sit through the volatility. Bet on the country that has spent 250 years turning problems into new growth cycles.

Happy Fourth of July.

Trading in Taxable Accounts: Is It Worth It?

A version of this story shows up every April. A client, call her Susan, gets a call from her CPA. Her equity strategy was up more than expected, and the tax bill was bigger than she planned for. The CPA asks a reasonable question: would she have been better off in a muni bond portfolio? Susan is upset. Not because she lost money. Because the check to the IRS feels like a loss.

Once a portfolio prints a new high, the mind anchors there. Any tax bill that reduces it feels like a loss from the peak rather than the cost of a very good year.

Here's what to remember. Gains are a win. A bigger tax bill is often the receipt for a bigger return.

To see how you're really doing, do a little apples-to-apples math. A 3% high-grade municipal bond yield at 0% federal tax is a 3% take-home. A 12% gross swing trading strategy taxed at 40% is 7.2%. The active strategy still wins, but by a smaller margin than the headline return implies. Two other variables tighten the comparison.

Holding period. Long-term capital gains, on positions held more than a year, are taxed at 15% or 20% federal. Short-term gains and most active-strategy distributions are ordinary income, running 32% to 37% for high earners.

State of residence. A Californian in the top bracket giving up a 3% in-state muni is really giving up closer to a 6.5% taxable-equivalent yield, since the muni is exempt from both federal and California tax. A Floridian or Texan in the top bracket is giving up roughly 5%. The lower the state tax, the smaller the muni free lunch.

At the end of the day, net returns are paramount when comparing investment strategies, because only the net compounds. The gross is a number. The net is what buys your next decade.

Bitcoin Thesis To Own

We sold most of our Bitcoin (BTC) late last year. Not because we lost faith. Because the tape started rolling over and a stack of technical exhaustion signals told us the easy money had already been made.

Selling into strength was the easy part. Buying it back when nobody wants it is the hard part.

Last week, we bought Bitcoin and a basket of crypto-related equities across Silverlight managed portfolios. Here is what pulled us back in.

On July 1st, the Crypto Fear and Greed Index closed at 11 out of 100. Extreme Fear. Bitcoin was trading near $58,800, roughly 53% below its October 2025 all-time high of $126,198. Money was fleeing crypto and piling into AI and semiconductor names with both hands.

Fear does not whisper at bottoms. It rings a bell. Our job is to be close enough to hear it and calm enough to answer. Three of those bells recently rang for Bitcoin, and they tend to ring together only near real lows.

The Puell Multiple tracks miner revenue against its 365-day average. It has dropped into the zone that historically marks the tail end of bear phases, when miners are squeezed. The MVRV Z-Score sits at 0.25, closing in on the historic accumulation band that has marked prior cycle lows. And DeMark 13 exhaustion signals printed across multiple timeframes. Three respected bottom tells, all pointing the same direction, at the same time.

None of these are magic, and nothing guarantees a bottom. But the technical picture for BTC has clearly improved from earlier this year, and we think the odds of at least a tradable low around current levels are good.

Silverlight managed accounts are currently long IBIT, MSTR, BITX, and ETHA.

Watching Walter Run

Soldier Field, November 13, 1977. Bears down 17-0. Walter Payton takes a sweep right, gets cut off, spins back into a wall of red jerseys. He breaks Willie Lanier's tackle. Then Tim Gray's. Three more Chiefs miss. Two more get bowled over. Half the Kansas City defense had a hand on him and none could put him down. Seven broken tackles, eighteen yards, a stadium on its feet. Bears won 28-27.

Payton stood 5'10" and played at 200 pounds in a league full of linebackers who outweighed him by a lot. Yet he ran without fear or hesitation. He would lower his shoulder into defenders twice his size and drag them for extra yards on sheer will. On that eighteen-yard run he ran through men who should have stopped him, because he never played like a man who expected to be.

Two years earlier, that same runner had a very different Sunday. September 21, 1975. Payton's NFL debut against the Baltimore Colts. Fourth overall pick in the draft. The Bears' franchise savior. He carried the ball eight times and gained zero net yards. Zero. He had missed most of training camp with an elbow infection and showed up under-conditioned. The Chicago newspapers said what Chicago newspapers say. His rookie season ended with 679 yards and seven touchdowns, which was fine, and forgettable, and nothing like what he had been drafted to be.

He could have gone quiet the way a lot of top picks go quiet. He did the opposite. He studied the film. He rebuilt the body. Two years later he led the NFL in rushing with 1,852 yards, and the eighteen against the Chiefs became the most famous run in franchise history.

Garry Kasparov once described peak performance as a paradox. "The eternal paradox," he wrote, "is how to learn from your failures while still carrying on as if you are invincible. You must learn and forget simultaneously." After a loss, you sit with the mistake, name it, study it, and extract every lesson the failure has to teach. Then you walk to the next board and behave as if the loss never happened.

The player who only broods becomes tentative. The player who only forgets keeps making the same blunder. The one who wins learns to do both at the same time.

The way Walter Payton ran the football is a working metaphor for how to move through life. The tacklers are the setbacks anyone faces trying to do something hard. The mental model is simple: never go down easy.

Elon Musk says, "Failure is irrelevant unless it's catastrophic." Hard to argue with that. Just ask Thomas Edison.

Fear of failure stops more people than failure ever will.

If you want to run like Walter in your own life, be the one willing to take the hits. Stay upright. Learn to bob and weave on your way to the end zone.

The end zone is not for the untouched. It's for the ones who keep moving.

This material is not intended to be relied upon as a forecast, research or investment advice. The opinions expressed are as of the date indicated and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and non-proprietary sources deemed by Silverlight Asset Management LLC to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Silverlight Asset Management LLC, its officers, employees or agents. This post may contain "forward-looking" information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any of these views will come to pass. Reliance upon information in this post is at the sole discretion of the reader.