5 Things We Learned This Week - 11/9/2025

November 9, 2025

The S&P 500 fell 1.6% this week. The Bloomberg Aggregate Bond Index was flat, Gold rose 0.1% and Bitcoin declined 5.5%.

This week’s data gave a mixed read on the U.S. economy. Consumer sentiment fell to 50.3, below forecasts, amid worries over the government shutdown and weaker personal finances. The ISM Services PMI rose to 52.4, with strong new orders and rising prices. Manufacturing PMI slipped to 48.7, showing ongoing contraction, though input prices dropped. ADP reported +42,000 jobs, topping estimates. Overall, solid services and hiring support growth, but weak sentiment and manufacturing may keep the Fed cautious on rates.

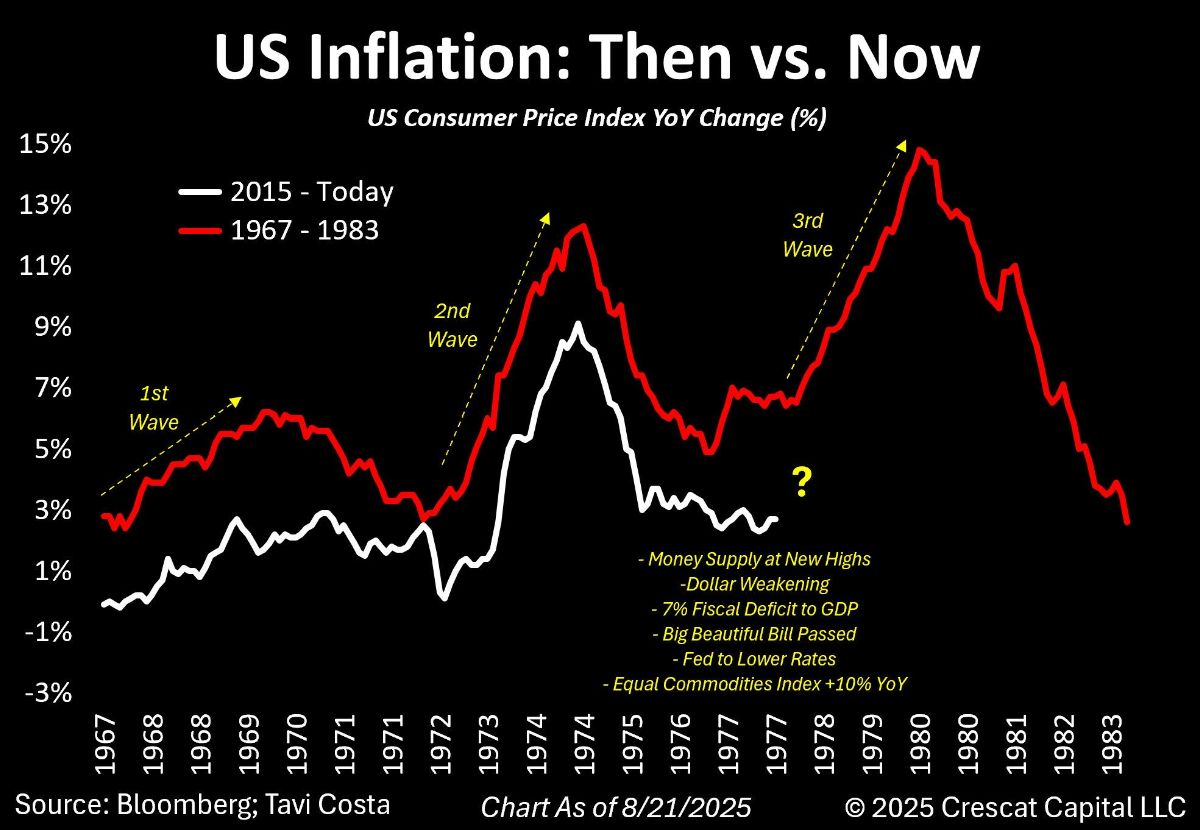

Just As Inflation Is Cooling, Here Comes Another Stimulus

Inflation comes in waves, and we might be on the verge of another upturn.

This weekend, President Trump announced a new "tariff dividend" — stimulus checks of at least $2,000 per person , excluding high-income households. Based on prior income cutoffs ($75K single, $150K married), roughly 220 million Americans, or 85% of adults, will qualify. That’s more than $400 billion in direct payments — one of the largest cash handouts in history.

The timing couldn’t be stranger. The economy is near full employment, AI-related capex is booming, the S&P 500 hovers near all-time highs, and yet Washington plans to pump hundreds of billions into consumer pockets. Meanwhile, the U.S. deficit jumped $345 billion in August alone, nearly 10 times larger than the $30 billion in tariff revenue funding these checks. This is the opposite of fiscal prudence.

Americans should think twice before celebrating another “free” check. Overstimulating an already hot economy risks reigniting inflation. Remember 2021? Millions spent their stimulus money fast, but years later they’re still paying higher prices for groceries and McDonald’s.

In reality, stimulus checks are like involuntary taxes—you pay them back through inflation. In the late 1970s, prices surged again after an initial cooldown. If history rhymes, 2026 could mark inflation’s next wave higher.

50-Year Mortgages Aren't The Answer

President Trump recently floated the idea of introducing 50-year mortgages to address soaring housing costs, posting on Truth Social an image comparing his proposal to FDR's 30-year loan. While well-intentioned, this misses the mark on America's deepening housing affordability crisis.

The root issue is that homeownership has become prohibitively expensive. Buyers now devote 38.6% of household income to mortgage costs—near record lows in affordability, akin to the 2006 bubble and well above the long-term average of 28%. High prices, driven by supply constraints, broken zoning laws, and institutional investors snapping up homes, have detached from wages, pushing the price-to-income ratio to 5:1 from a historical 3:1.

Extending mortgage maturities sounds appealing but does little good. On a $400,000 loan at 6%, a 50-year term saves just $166 monthly versus 30 years. Meanwhile, interest balloons to $863,000 from $418,000—doubling the cost. Equity builds glacially, with early payments mostly interest, leaving borrowers wealth-poor longer. Lenders may add 0.3-0.5% in rates, erasing savings.

A better path: The federal government should cease interventions and let markets clear. Prices must decline or stagnate while incomes rise. Debt isn't the solution—it's a liability that impoverishes individuals and nations alike. True reform demands supply-side fixes, not more borrowing at longer maturities.

AI Sucks At Investing

In the inaugural Alpha Arena contest, a high-stakes showdown took place between six powerhouse AI models. Heavyweights like Grok, Claude, and Gemini were each handed $10,000 to duke it out in crypto trading. Over two intense weeks, they navigated the wild swings of Bitcoin, Ethereum, and other digital assets.

The result? A spectacular flop. Four models tanked hard, hemorrhaging 30% to 63% of their funds, while just two scraped by with meager single-digit gains. This crypto carnage exposes AI's investing limitations. Several factors hobble AI's investing ability, including: overreliance on historical patterns, failing to predict black swan events, inherent biases like eternal optimism, collapse under market complexity and unstructured data, user skill atrophy, and herd effects from uniform models.

The takeaway is to treat AI as a sidekick—not the driver when it comes to executing important tasks. Recent legal fiascos illustrate the point further. A California lawyer was recently fined $10,000 for filing an appeal with 21 fake citations generated by ChatGPT.

Palantir Is A Valuation Trap Created By Vanguard

We usually focus story #4 on a stock Silverlight clients own. This week, we wanted to profile a stock we don't currently have a position in.

Palantir Technologies (PLTR) was founded in 2003 and is headquartered in Denver, Colorado. The company specializes in data analytics software. Over the last couple of years, PLTR stock has skyrocketed, delivering annual returns of 167% in 2023, 340% in 2024, and 131% so far in 2025. This explosive appreciation far outpaces the company's fundamentals: revenue grew about 23% annually from 2022-2024 before accelerating to around 50% growth in 2025. The stock's surge appears disconnected from these metrics, running well ahead of actual business growth.

PLTR is literally a valuation monster. If Vanguard was a mad scientist, PLTR could be its Frankenstein. The stock trades at a P/E ratio of 424 and a P/S multiple of 107. By comparison, the broader S&P 500 index trades at a P/E of 26 and P/S of 3.5.

PLTR joined the S&P 500 on September 23, 2024. At inclusion, its market cap was around $84 billion, ranking it approximately 100th in the index. Today, with a $424 billion market cap, it ranks 20th.

Making the jump from #100 to #20 in the S&P 500 is a really big deal, because it allows PLTR to suck in a lot more passive flows. Similar to Tesla in 2020, getting added to the index generated a lot of positive stock momentum for PLTR last year. Once a stock has that kind of momo and the passive machine gets a hold of it, fireworks are possible. That's because firms like Vanguard and Blackrock, which run most of the country's retirement portfolios, mechanically buy more shares as prices rise. They disregard traditional value metrics—like P/E ratios—that investors learned to appreciate after the Great Depression exposed the hazards of speculative excesses.

To justify today's prices, PLTR investors must assume an irrational rate of growth. PLTR would have to continue to grow at a 50% CAGR for many years. Few companies grow like that in perpetuity. Hyper-valued stocks like PLTR can be traded, but we don't think they are a wise long-term investment.

Time Is Finite, Spend It Wisely

At the age of 82, an Italian woman named Bianca told her neighbor she would “give up two years of my life to spend one afternoon with my mum and dad.”

She regretted not sitting with them more, not hearing their stories, not telling them one more thing. “So many times when I go to bed I kiss their photo. I say, ‘I wish you were here. Even for just one day.’”

Tim Urban’s “Your Life in Weeks” poster is a grid of 4,680 tiny boxes, one for each week in a 90-year life. Flip the lens to family, and the math gets compelling.

If your parents are 70, you likely have ~1,000 weekends left with them.

If your child is 10, you have around 416 weeks until college.

If your child is 15, you have around 156 weeks until college.

So how about looking at time itself as the most important ROI? Or, the Return on Relationships?

There are countless ways to do this. For example, you could start a tradition of Friday lunches with parents. Data shows shared meals correlate with 24% lower mortality risk in seniors. Or, schedule a recurring Facetime meeting every Sunday.

Kids spell love: T I M E. Harvard’s 85-year Grant Study proves cumulative hours spent together mean more than perfectly curated moments. So try out a weekly “device-free dinner,” or plan a series of overnight trips with no agenda other than fun and exploration.

Audit your calendar like a portfolio. Reallocate 5% of your hours to the most irreplaceable assets - your loved ones.

This material is not intended to be relied upon as a forecast, research or investment advice. The opinions expressed are as of the date indicated and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and non-proprietary sources deemed by Silverlight Asset Management LLC to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Silverlight Asset Management LLC, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any of these views will come to pass. Reliance upon information in this post is at the sole discretion of the reader.